Bulloch County is currently considering the proposal of a pension plan for full-time employees.

The county commission held a work session on August 3 with a committee of county employees present. The committee was assembled to consider pension plan options, and each county department was represented.

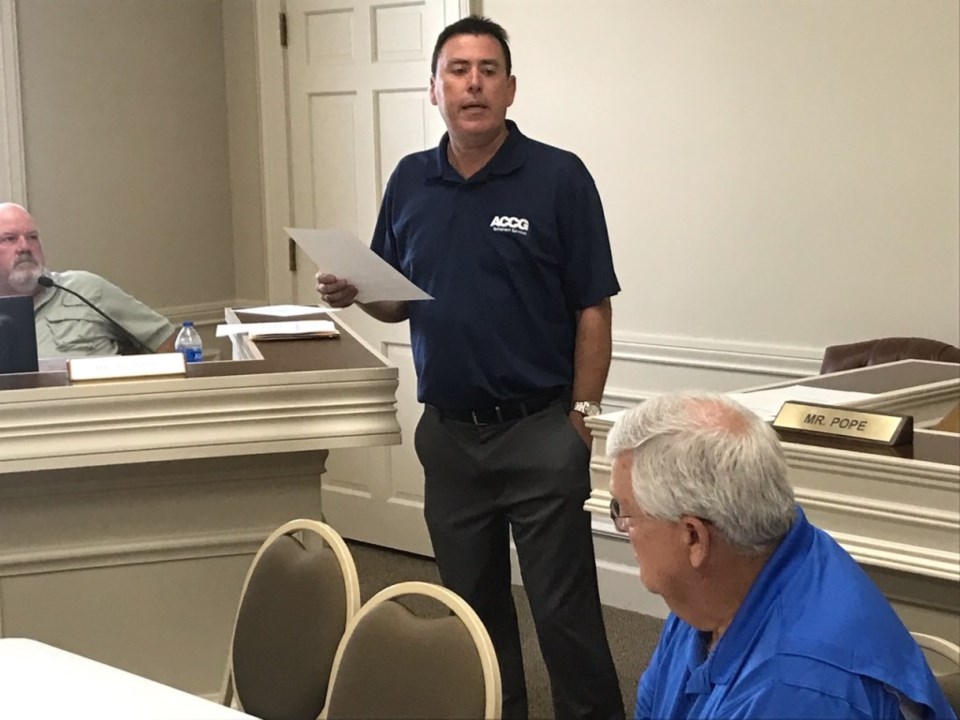

The county currently offers a 401(a) plan, which is a defined contribution plan. In contrast, the pension is a defined benefit plan. Greg Gease, a representative from ACCG Retirement Services, prepared the plan options and presented them at the work session.

What are the differences between the current 401(a) plan and a pension plan?

401(a) Plan

With the 401(a), full-time employees receive a retirement benefit directly correlated to the amount they have contributed to the plan during their working years. In short, the more money the employee and employer (through matching) contribute to the plan, the better the investments will perform and the more money the employee will collect upon retirement.

The 401(a)’s value is affected by the amount of money contributed, rather than the employee’s age, years of service, or salary. In this plan, the employee assumes most of the responsibility for contributions.

Upon the employee’s retirement, he or she is entitled to the sum of money in their retirement account. That money is also transferable to a beneficiary on the employee’s death, whether before or after retirement.

Pension Plan

In contrast, a pension plan offers a defined retirement benefit that does not fluctuate between employees. Instead, it is calculated based on a set salary multiplier and retirement age, similar to social security benefits.

The benefit is, therefore, determined by the employee’s years of full-time service. It is a deferred, vested benefit.

Rather than a lump sum upon retirement, a pension is paid out in a guaranteed monthly benefit for the remainder of the employee’s life. Upon death, the payments will end. The employee does have the option to attach their spouse to the pension plan when setting it up. The spouse would then receive a monthly benefit after the employee’s death.

If the county were to institute a pension, employees would always have the option to save on their own through their tax-deferred 457 plan. Currently, the county offers matching contributions to those plans, but Gease said matching is typically not offered for 457 plans if the employer also offers a pension.

What are the pension options, and what funding is needed?

ACCG prepared several different plans for the county to review. The plans varied based on the salary multiplier percentage and the standard retirement age.

The company’s actuarial team conducted a cost study at both a 1.5 percent and 1.75 percent salary multiplier and standard retirement ages of 62 and 65.

For every year of full-time service, that percentage of an employee’s salary would be replaced in their pension fund. This means that the more time an employee serves at the county, the more their pension is going to replace in retirement.

The pension plan also comes with the ability for the employer to add options or additional benefits, which can make the plan more expensive to fund.

For the pension funded at 1.75 percent with a retirement age of 62, the projected cost to the county is $29 million. To fund the pension at 1.5 percent with a retirement age of 65, the projected cost is $22 million.

How would the pension be funded?

One option for funding the majority of the plan is for current employees to use their existing 401(a) funds to “buy back” their years already worked. They can then vest those in their pension instead. This would be an election on the part of employees and not mandatory. They may also choose to retain their 401(a) balance and switch to the pension; however, only their years of service following the switch would be vested.

The current reserve in county-wide 401(a) funds is $20 million. So if all employees elected to move to a pension plan and buy back their time, this would leave the county with unfunded pension liabilities of around $2 million for the cheaper plan and around $9 million for the more expensive plan.

The unfunded liability is not due in a lump sum; the county would pay it over time. The county commission would determine how to best fund the pension.

The county must fund the pension annually, as regulated by the state. The cost of the pension is estimated but can vary based on market growth. Any losses are spread out over time, while any gains are credited to the county for future payments. If at any time the pension is not being funded, the state notifies all employees.

Gease noted that the adoption of a pension plan is a “long-term relationship” that would be more difficult for the county to get out of, should they adopt it and decide to leave it in the future.

However, the county could choose to reduce benefits within the pension in the future, such as lowering the salary multiplier percentage, in an effort to reduce costs. The county can never take away what an employee has already vested into his or her pension.

Which is the better plan? It depends.

ACCG’s Gease described comparison of the plans as “apples and oranges,” as each can vary based on outside factors, which can be unpredictable, as well as an employee’s personal preferences. He also noted that the county’s choices on how to fund either plan will affect its value.

He described the basic difference as a finite sum in an account upon retirement (the 401(a) plan) versus a check in a set amount each month for the rest of one’s life (the pension plan).

There are many moving parts within each plan that can affect each employee differently. Gease offered several hypothetical calculations based on employee age at retirement, years of full-time service, salary multiplier rates, extra options, and social security benefits to demonstrate the variations in 401(a) or pension pay-outs that different employees could expect.

Because there is such significant variation between employees, he would not name either plan as the “better” option across the board.

What do county employees think?

Captain Marcus Nesmith, a member of the Bulloch County Sheriff's Office Crime Suppression Team, chaired the committee reviewing the plans. The committee members sought feedback from their fellow employees across departments.

“A majority of employees we’ve talked to want to go to a pension,” he said. “With a pension, someone will sit down with you and say, ‘This is what you’ll get in a check every month.”

He also noted that the current 401(a) system does allow for the passing on of “generational wealth,” but it also requires more responsibility and money management on the part of the employee.

“Eventually the [401(a)] account will run out, but a pension won’t,” he said. “I think it’s the comfort of knowing what you’ll get every month.”

Others in the work session noted that the offer of a pension is attractive to potential new employees, especially those in the public safety sector. This could be an important recruitment tool for Bulloch County.

What are the next steps?

During the work session, the county commission expressed an interest in choosing the details of a particular pension plan before entering a due diligence period. During that time, they would be able to research the specific plan and make a more informed decision prior to voting on whether to move to a pension.

With that being said, they agreed to move forward on researching the least expensive option – the pension with a 1.5 percent salary multiplier and a standard retirement age of 65.

Again, that would be a cost of approximately $22 million to Bulloch County, $20 million of which could be covered by current 401(a) funds.

Several commissioners, including Chairman Roy Thompson, noted that they were not in favor of raising taxes to cover a new benefits plan for county employees.

Grice Connect will provide a follow-up when additional decisions are made about the pension plan.